What is Fraud? Meaning, Examples, Types & Prevention Guide 2025

Every year, millions fall victim to clever tricks disguised as opportunities, official messages, or even genuine transactions. But one small click or casual signature can quickly snowball into drained bank accounts, stolen identities, or shattered trust. Fraud today wears many faces, and no one is completely safe from it.

In this guide, you’ll uncover what fraud really means, explore real-world examples, learn about different types of scams, understand why they happen and discover how to protect yourself in a fast-changing digital world.

What is Fraud?

Fraud is a misleading or deceptive act committed by an individual, group, or organization with the intent to gain an illegal advantage or harm another person’s rights. It often involves manipulation, concealment, or false representation of facts for personal or financial benefit. Examples include credit card fraud, bankruptcy fraud, securities fraud, and wire fraud, all designed to exploit trust and cause loss to the victim.

What are Scams?

A scam is a dishonest scheme designed to trick people into giving away money, personal data, or valuable information. It is a type of fraud. Scams appear in many forms, such as fake investment offers, phishing emails, online shopping fraud, or lottery winnings that sound “too good to be true.”

In short, scams are fraudulent traps created to exploit trust for quick financial gain.

What is Cyber Crime?

Cybercrime is any illegal activity carried out through digital devices or the internet, targeting individuals, businesses, or governments. It involves hacking, identity theft, ransomware, phishing, data breaches and financial fraud. Cyber criminals exploit weak passwords, fake websites, and social engineering tricks to access confidential information or money.

Unlike traditional crimes, cyber crimes are borderless; a hacker sitting miles away can attack your bank account or company systems within seconds. As technology becomes more integrated into daily life, cybercrime continues to evolve, making awareness and digital vigilance more crucial than ever.

Types of Fraud & Scams

Below are some of the most common types of fraud and scams you should know:

Why Does Fraud Happen?

Fraud doesn’t just happen by chance; it’s driven by a mix of motivation, opportunity, and rationalization. People commit fraud when they feel financial pressure, see a loophole they can exploit, or convince themselves that “no one will get hurt.” Weak internal controls, lack of awareness, and digital vulnerabilities also create perfect conditions for fraud to thrive.

Sometimes it’s pure greed; other times, it’s desperation or misplaced trust. Whether it’s a corporate insider manipulating accounts or a scammer exploiting emotions online, fraud ultimately happens when ethics break down and opportunity meets temptation.

Recent Fraud Examples (2025)

Operating from a rented house, he posed as a government official, lured victims with false promises and reportedly amassed over ₹300 crore. His network even spanned multiple countries, with more than 160 foreign trips made to launder money through hawala routes.

Massive and Regular Frauds

Massive frauds are large-scale, organized crimes that cause heavy financial losses, often running into crores or even billions. These are usually planned by groups or corporate insiders with access to resources and authority. Examples include bank scams, corporate accounting frauds, government fund embezzlements, and major cyberattacks.

Such frauds often go undetected for years and shake public trust once exposed. They damage reputations, economies and entire systems built on credibility.

Regular frauds , on the other hand, are smaller but far more frequent. These include phishing messages, fake calls, lottery scams, and online purchase fraud. Though each case may seem minor, together they cause massive cumulative losses every year. What makes regular fraud dangerous is its accessibility.

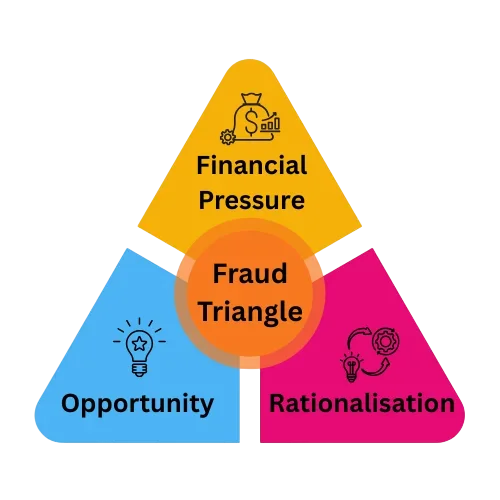

Fraud Triangle

The Fraud Triangle is a classic model that explains why people commit fraud. Developed by Dr. Donald Cressey, the model identifies three driving forces that come together when fraud occurs:

Removing even one side of the triangle (like tightening controls or reducing pressure) can significantly reduce the risk.

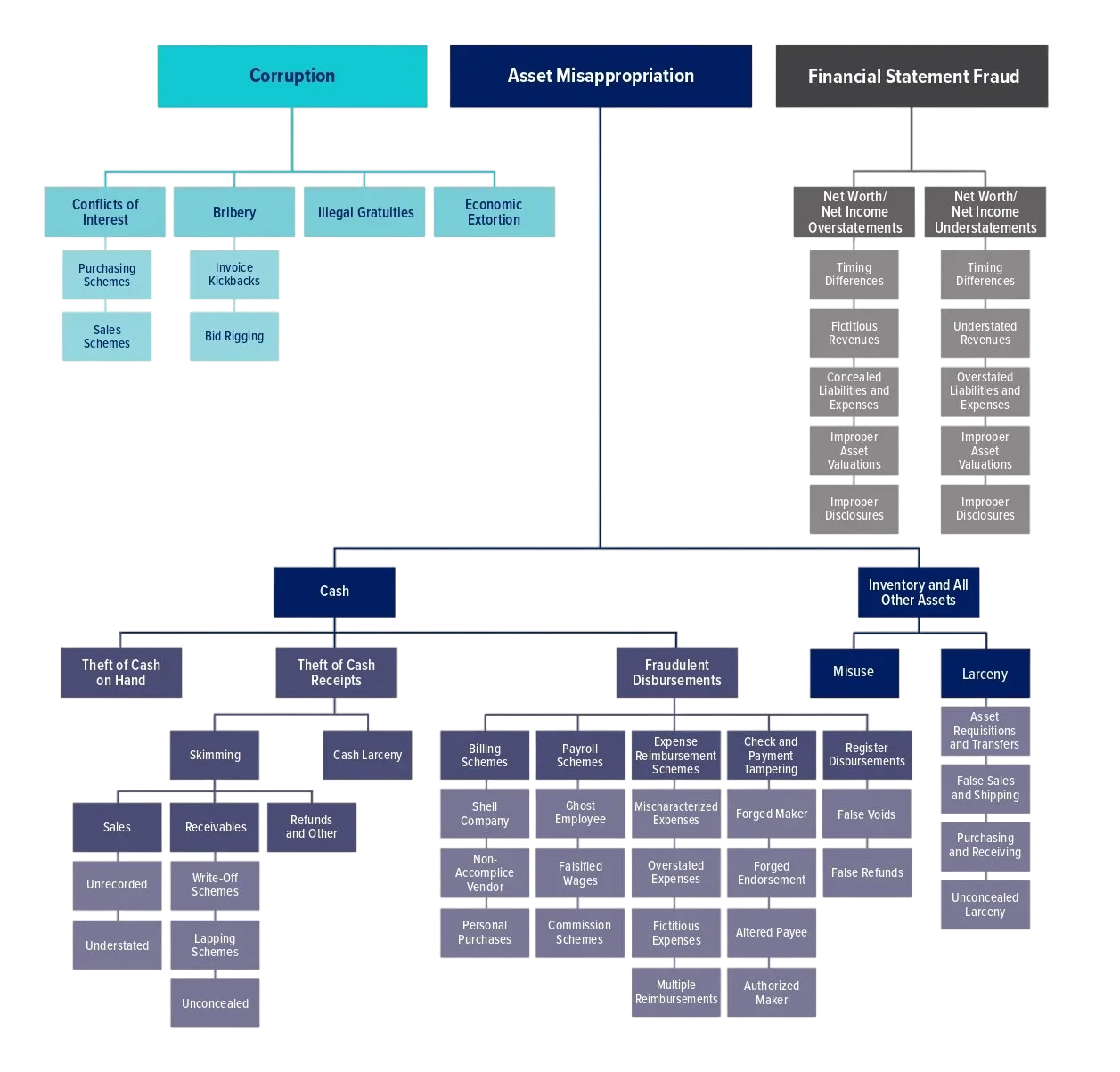

Fraud Tree

The Fraud Tree is a detailed framework that classifies different types of fraud systematically. It helps investigators, auditors, and organizations understand how fraud happens and what form it takes. Much like a real tree, it branches out into three main categories:

Examples of corruption include Bribery, Conflict of Interest, Illegal Gratuities & Economic Extortion.

Examples include cash theft, payroll fraud, expense reimbursement manipulation, or inventory theft.

Examples include Overstating Revenue, Understating Expenses & Improper Asset Valuation

Fraud Laws & Penalties

1. Criminal Cheating (Indian Penal Code / Bharatiya Nyaya Sanhita)

Cheating (formerly IPC Section 420; now recast under the new penal code provisions) covers dishonest inducement to deliver property or alter documents. Convictions typically carry prison terms and fines; the law treats deliberate deception as a serious criminal offence. This is the go-to provision for many classic frauds (fake sales, false promises, forged documents).

2. Money-Laundering (PMLA - Prevention of Money Laundering Act)

When fraud proceeds are “cleaned” through bank transfers, shell companies, hawala, or other layering tactics, PMLA applies. It authorises attachment/confiscation of assets derived from fraud, prosecution and long prison terms. Enforcement agencies (ED) use PMLA to follow the money and recover illicit wealth.

3. Corporate & Financial Statement Fraud (Companies Act - Section 447 / Corporate Offences)

Intentional manipulation of books, false disclosures, or misstatements to mislead shareholders is a specific corporate offence. Penalties can include heavy fines, imprisonment for responsible officers, and disqualification from company management; courts treat fraud in the public interest more severely.

4. Cybercrime & Digital Fraud (Information Technology Act / Computer-related Offences)

Hacking, phishing, ransomware, and online financial fraud are dealt with under IT Act provisions (e.g., computer-related offences) and specific penal code sections. Penalties range from fines to multi-year imprisonment, plus interim remedies like blocking or takedown of fraudulent sites and freezing of accounts.

5. Securities & Market Fraud (SEBI Regulations & Insider Trading Rules)

Market manipulation, insider trading, and false disclosures fall under SEBI’s regulatory framework. SEBI can impose disgorgement (return of illegal gains), heavy fines, market bans (suspension from trading or board positions), and coordinate with criminal agencies for prosecution. Recent regulatory updates (2025) have tightened definitions and penalties for insider trading and UPSI violations.

6. Tax & GST Frauds (Income-tax/GST Laws)

False returns, bogus invoices and fake input tax credit claims attract income-tax and GST penalties. Besides fines and prosecution, tax authorities routinely initiate searches, provisional attachment of bank accounts, and recovery proceedings, often coordinated with criminal investigations when fraud is deliberate.

7. Banking & Financial Frauds (RBI / Banking Laws)

Unauthorized transactions, cheque/ATM fraud and loan fraud trigger banking regulations. RBI and banks may reverse unauthorized debits, but large systemic frauds lead to probes, penalties on institutions for supervisory lapses, and criminal referrals.

8. International & Cross-border Remedies

For scams that cross borders (offshore accounts, shell companies abroad), Indian enforcement agencies coordinate with foreign authorities, use mutual legal assistance treaties (MLATs), and rely on asset-tracking laws like PMLA to secure recovery.

Typical Remedies for Victims of Frauds & Scams (what the law enables you to do)

Penalties - What offenders typically face

Penalties vary by statute but commonly include: imprisonment (years to decades for severe offences), heavy fines or disgorgement of gains, confiscation of assets, market bans, disqualification from holding corporate office, and civil damages paid to victims. Repeat or large-scale offenders face the harshest consequences.

Why enforcement can be slow, and what it means for victims

Complex frauds (layered transactions, cross-jurisdictional trusts) require lengthy financial forensics, mutual legal assistance, and court proceedings, which explains slow conviction rates even when investigations are numerous. Victims should therefore act fast (preserve records, report early) to improve chances of recovery.

Who Investigates Fraud?

Fraud investigations involve multiple specialized authorities, depending on the type and scale of the crime. Here’s who typically investigates fraud:

1. Law Enforcement Agencies

National and local police departments handle most criminal fraud, such as identity theft, online scams, or business fraud. They collect evidence, file FIRs or reports, and work closely with cyber and financial crime units.

2. Financial Regulatory Bodies

Organizations like RBI (India), SEBI, FBI, SEC (U.S.), or FINRA oversee financial markets and corporate transactions. They monitor suspicious patterns like insider trading, accounting manipulation, or money laundering.

3. Cybercrime Units

These are specialized teams under national law enforcement that investigate hacking, phishing, ransomware and digital payment fraud. They often collaborate with tech firms and cybersecurity experts to track digital footprints and recover stolen data.

4. Corporate Compliance Teams

Large companies have internal audit and compliance departments responsible for detecting and preventing fraud early. They conduct internal investigations before external authorities step in.

5. Certified Fraud Examiner (CFE)

Certified Fraud Examiners (CFEs) are the detectives of the corporate world. They identify suspicious transactions and trace how and where fraud actually happens. They play a critical role in detecting fraud in banks, corporates, consulting firms, insurance companies, government agencies and even law enforcement units. CFEs combine skills from auditing, investigation, finance and law to connect every missing link in a fraud case.

CFEs are in high demand to safeguard the finances and internal controls of organizations as fraud is rising in the upcoming era. The scope for CFEs is massive, from forensic accounting and compliance audits to cyber fraud detection and risk management. If you are exploring this career, it also helps to understand potential earning growth with a detailed view of Certified Fraud Examiner salary trends in India and globally

To become a Certified Fraud Examiner, you just need to clear the CFE certification exam, which tests your understanding of fraud prevention, detection and investigation. Preparing under expert guidance gives you a huge edge and that’s where the Academy of Internal Audit (AIA) steps in.

When you plan your journey, make sure you know the complete CFE exam fees and retake policy so there are no surprises in your budget.You should also decide early whether you will take the CFE exam from home or at a Prometric test center, because the requirements and experience for both options are slightly different.

If you want to go deeper into the legal side of fraud, module-wise resources like CFE Module 2 – Law explain offences, evidence rules and key regulations in a structured way. As you get closer to the exam, you can boost your preparation using proven strategies to unlock your CFE exam success from time management to question practice.

For students specifically targeting the investigation and fraud schemes side, advanced content such as CFE Module 4 can sharpen practical skills relevant to real-world fraud cases.

AIA’s specialized CFE Prep Program offers structured practical training, real-world case studies and mentorship from industry experts to help professionals implement skills in the real world offers structured learning.

Fraud in Business vs Personal Life

Fraud can creep into both professional and personal spaces, but the motives, impact, and warning signs often differ.

1. Fraud in Business

Business fraud occurs when someone within or outside an organization deceives the company for financial advantage. This includes embezzlement, procurement scams, fake vendors and misreporting accounts.

Example: A finance manager creates fake invoices to siphon money, or a vendor inflates bills to earn illegal profits. Such frauds harm a company's reputation, investor trust, and financial stability.

2. Fraud in Personal Life

Personal fraud affects individuals directly, from online shopping scams to credit card theft. Scammers manipulate emotions, urgency, or ignorance to steal money or personal data.

Example: Receiving fake bank calls asking for OTPs, phishing links, or lottery messages claiming rewards. These scams exploit human psychology more than technology.

Small Business Fraud Examples

Small businesses often face fraud from within - usually by employees or vendors who exploit weak internal controls. For example, an employee might create fake expense reports, divert customer payments, or manipulate invoices for personal gain. Vendors may also overcharge or supply poor-quality goods while billing full rates.

These frauds may seem small, but they can severely affect cash flow and trust. Regular audits, clear approvals, and segregation of duties can prevent such incidents.

Personal Banking Fraud

Personal banking fraud happens when someone illegally accesses your bank information to steal funds or misuse your financial identity. This includes phishing emails, fake loan calls, cloned debit cards, UPI scams, or fraudulent investment apps. For instance, scammers might pose as bank representatives, tricking victims into sharing OTPs or login credentials. Others use phishing links or malware to capture card details and execute unauthorized transactions.

The best defense is awareness. Never share personal banking details, always verify sender authenticity, and immediately report suspicious activity to your bank.

Protect Yourself from Fraud

Here’s how you can safeguard your money, data, and identity from fraud:

1. Verify Before You Trust: Never share your personal or banking details with anyone claiming to be from a bank, government, or company. Always confirm the identity of the caller or sender through official channels.

2. Keep Your Devices Secure: Use strong passwords, enable two-factor authentication (2FA), and update your devices regularly to prevent hacking or malware attacks.

3. Monitor Financial Transactions: Regularly check your bank statements, credit card bills and UPI logs. Report any unauthorized or suspicious transactions immediately.

4. Be Cautious of Online Links & Offers: Avoid clicking on links or attachments from unknown sources. Fraudsters often disguise phishing emails as official communication from banks or e-commerce sites.

5. Secure Business Operations: If you run a business, conduct background checks on employees and vendors, implement approval hierarchies, and audit accounts frequently.

6. Educate Your Team & Family: Train employees and family members about common scam tactics like fake OTPs, suspicious links, or urgent payment requests. Awareness is your strongest defense.

7. Use Reputed Platforms: When investing, shopping, or transferring money online, use verified and trusted platforms only. Always look for “https://” and secure payment gateways.

8. Report Fraud Immediately: If you fall victim, don’t panic; report the incident to your bank, local police, or cybercrime cell immediately. Quick reporting can stop further losses and help trace the fraudster.

Conclusion :

Fraud has evolved from paper-based scams to sophisticated cybercrimes. Understanding how fraud works, why it happens, and how to prevent it is important.

That’s where education and expertise make all the difference. Professionals trained in fraud detection and prevention, especially Certified Fraud Examiners (CFEs), are leading the global fight against financial deception.

If you aspire to build a rewarding career in fraud investigation, the Academy of Internal Audit (AIA) can help you get there. Through structured learning, mentorship, and globally recognized CFE preparation programs, AIA empowers learners to turn knowledge into impact, helping organizations stay ethical, transparent, and fraud-free.

FAQ :

1. What are three common types of fraud?

The three most common types of fraud are financial fraud, identity theft, and cyber fraud, each involving deception for personal or financial gain through manipulation or false representation.

2. What is fraud in 2 marks?

Fraud means intentionally deceiving someone to gain money, property, or advantage by unfair or illegal means. It involves dishonesty, misrepresentation, and breach of trust.

3. What are the 4 factors of fraud?

The four key factors of fraud are pressure, opportunity, rationalization, and capability, together explaining why and how individuals commit dishonest acts for personal benefit.

4. What is high-level fraud?

High-level fraud refers to large-scale deception involving senior management or powerful individuals, often leading to significant financial losses, corruption, and damage to public or corporate trust.

5. What are the six symptoms of fraud?

Six common symptoms include unexplained losses, unusual transactions, missing records, lifestyle changes, altered documents, and internal control overrides - early warning signs that demand immediate investigation.

6. How do fraudsters behave?

Fraudsters often appear overconfident, secretive, or controlling, manipulate trust, avoid scrutiny, and justify their unethical actions while trying to conceal their real intentions.

7. How to identify fraudulent people?

Fraudsters can be identified through inconsistent stories, hidden financial motives, sudden wealth, defensive behavior, and suspicious transactions that don’t align with their role or lifestyle.